12 Proven Life Insurance Sales Scripts to Close More Deals

Discover 12 life insurance sales scripts to boost your close rate. From cold calls to objection handling, these pitches work. Download our free PDF now!

TL;DR:

- Life insurance sales scripts are structured conversation frameworks that guide agents through prospecting, objection handling, and closing.

- This guide covers 12 scenario-specific scripts organized into four categories: prospecting, objection handling, demographics, and closing.

- Each script includes a psychological rationale, delivery format, and customization guidance for immediate field use.

- Supporting sections include an objection matrix, SMS and voicemail templates, and interactive video integration guidance.

- Download the free Life Insurance Script Swipe File to keep all frameworks accessible during live calls.

Who this is for: Life insurance agents, independent brokers, agency sales managers, insurance sales trainers, and team leads responsible for agent onboarding and script development.

According to the 2025 LIMRA Insurance Barometer Study, more than 100 million American adults say they need life insurance, and 37% intend to buy within the next 12 months. Many will not follow through without education, timing, and a clear next step. The barrier is almost never the product. It is the conversation.

Agents lose prospects at predictable moments: the opening that does not establish relevance, the objection that goes unacknowledged, the follow-up that never arrives. A structured script addresses each of these moments with a tested framework rather than an improvised response.

This guide provides 12 scenario-specific life insurance sales scripts organized into four operational categories. Each script includes a defined use case, a psychological rationale, and a customization note. Supporting sections cover objection handling, multi-channel follow-up templates, and how to use interactive video to turn these scripts into trackable sales flows.

Whether you are training new agents, refreshing a stagnant pipeline, or building a repeatable prospecting system, these frameworks are designed for field use.

For teams looking to move beyond static scripts, see how interactive video for agent training and turning static scripts into interactive video are changing how agencies build and deliver sales frameworks.

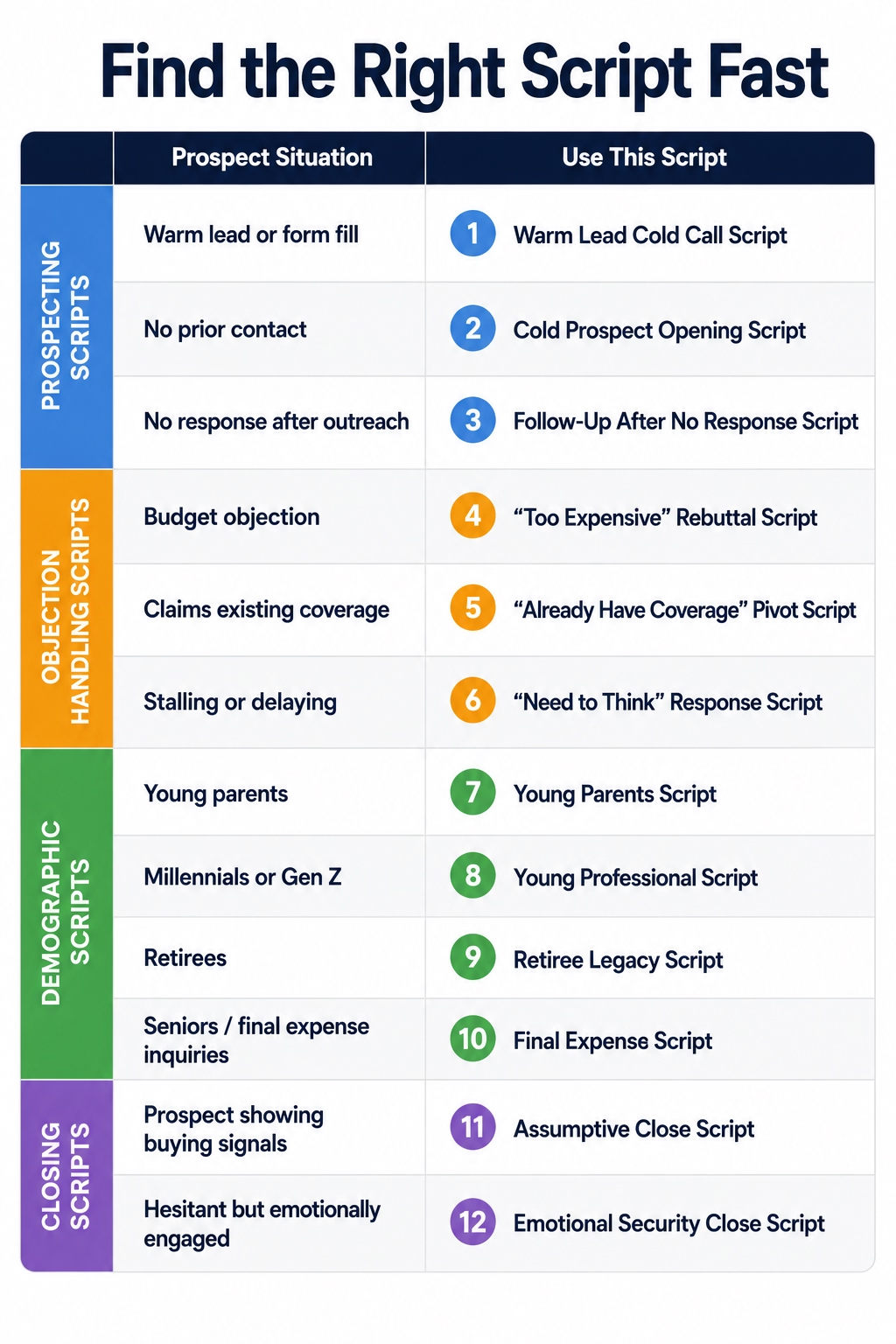

Find the Right Script Fast

Match your script to the prospect's current situation before the call begins. Each of the 12 scripts below targets a specific scenario, goal, and delivery tone for that interaction.

What Makes a Life Insurance Sales Script Effective?

Effective life insurance scripts work because they reduce agent hesitation, match the prospect's psychological state at each call stage, and provide clear mechanics for moving toward a next action.

Scripts alone do not close deals. The agent still needs to listen, adapt, and read the conversation. A well-built script reduces the cognitive load of deciding what to say next, which frees up mental bandwidth for actually hearing what the prospect is telling you.

According to the 2025 LIMRA Insurance Barometer Study, over half of Americans overestimate the cost of life insurance. The same research shows that 37% of consumers intend to purchase coverage within the next 12 months. That intent gap is where scripts operate. The prospect is already interested. The script is the bridge between interest and action.

Four elements determine whether a script converts:

Relevance to prospect context. A script aligned to the prospect's life stage, financial situation, or stated concern reduces the psychological distance between the agent's offer and the prospect's perceived need. Generic scripts produce generic resistance.

Objection anticipation. High-performing scripts include pre-built pathways for the most common resistance points. This reduces agent hesitation during live calls and signals preparation over improvisation.

Compression of credibility signals. Agents have limited time to establish authority. Scripts that incorporate outcome language (what the policy does for the prospect's family or estate) build trust faster than feature-focused language (what the policy contains).

Clear transition mechanics. Every script should move the conversation toward a defined next action: a scheduled call, a quote request, or a commitment. Scripts without explicit transition mechanics produce conversations that end without outcomes.

For agencies using Clixie, the same framework logic that makes scripts effective also determines how interactive video branches are structured. You can track how prospects engage with your video to identify which script segments produce the most friction or the strongest intent signals.

12 Life Insurance Sales Scripts by Scenario

The 12 scripts below are organized into four operational categories. Each script functions as a standalone framework with a defined use case, psychological rationale, and field-ready customization guidance.

Category 1: Prospecting Scripts

Script 1: Warm Lead Cold Call Script

Best for: Prospects who submitted a quote request, filled out a web form, or responded to a direct mail offer within the past 7 days.

Primary goal: Open a low-pressure conversation and establish a scheduled follow-up or immediate discovery call.

Why it works: Referencing the lead source activates recognition and reduces the cognitive dissonance between the agent's outreach and the prospect's prior action. Offering a timing choice gives the prospect perceived control, which lowers initial resistance and increases willingness to engage.

Script:

"Hi [Name], this is [Agent Name] with [Agency]. I noticed you recently requested some information about life insurance coverage options for your family. I wanted to reach out personally to walk you through a few plans that might be a good fit. Is now a convenient time, or would later today or tomorrow work better for you?"

Customization tip: Reference the specific lead source if available, such as "I saw you came across our family protection guide," to increase relevance and reduce cold-call friction.

Script 2: Cold Prospect Opening Script

Best for: Prospects with no prior engagement who match a demographic or behavioral profile, such as age range, homeowner status, or a recent life event.

Primary goal: Establish relevance within the first 15 seconds and earn 3 to 5 additional minutes of conversation.

Why it works: Leading with outcome language rather than product language bypasses the automatic resistance response triggered by product-first openings. Framing the call around the prospect's situation rather than the agent's offer shifts the psychological frame from interruption to inquiry.

Script:

"Hi [Name], my name is [Agent Name], and I work with families in [region] on life insurance coverage options. I am not calling to sell you anything today. I just want to ask two quick questions to see if there is a plan that might make sense for your situation. Do you have 90 seconds?"

Customization tip: Replace "families in [region]" with a more specific demographic signal if available, such as "homeowners in [city]" or "parents of young children."

Script 3: Follow-Up After No Response Script

Best for: Prospects who did not answer an initial call, did not respond to a voicemail, or went quiet after showing early interest.

Primary goal: Re-engage without creating pressure or implying frustration, and secure a specific callback time.

Why it works: A persistent but low-pressure follow-up maintains the agent's visibility without triggering the avoidance response that aggressive outreach creates. Offering a concrete scheduling option reduces the cognitive load on the prospect and makes responding easier.

Script:

"Hi [Name], this is [Agent Name] from [Agency] again. I tried reaching you a couple of days ago and wanted to try once more. I know life gets busy. I have a few coverage options I think could be a strong fit for your situation, and I only need about five minutes to walk you through them. Would [specific day] at [specific time] work for a quick call, or is there a better time I should reach you?"

Customization tip: Send this as a voicemail and immediately follow with the SMS version from the follow-up templates section below. Multi-channel outreach produces significantly higher contact rates than single-channel follow-up.

Category 2: Objection Handling Scripts

Script 4: "It's Too Expensive" Rebuttal Script

Best for: Prospects who respond to an initial pitch with price-based resistance before reviewing specific plan options.

Primary goal: Reduce financial resistance by validating the concern and redirecting toward affordable plan structures.

Why it works: Validating a financial objection before presenting alternatives reduces the prospect's defensiveness by signaling acknowledgment rather than dismissal. Introducing social proof through "clients who felt the same way" activates normalization, which lowers the perceived risk of continuing the conversation.

Script:

"That concern makes complete sense, and I hear it often. A lot of the clients I work with had the same reaction before we sat down together. What we usually find is that there are term life options starting at coverage levels most families can work into a monthly budget comfortably. Can I take five minutes to show you what a plan in your range actually looks like, just so you have a real number to compare against?"

Customization tip: Follow with a specific monthly premium example relevant to the prospect's age bracket. Concrete numbers reduce ambiguity and move the conversation from abstract concern to specific comparison.

Script 5: "I Already Have Coverage" Pivot Script

Best for: Prospects who deflect by claiming existing coverage, often without knowing specific policy details.

Primary goal: Open a non-confrontational coverage review conversation that surfaces potential gaps without dismissing the prospect's existing policy.

Why it works: Affirming the prospect's existing coverage removes the adversarial dynamic and positions the agent as an advisor rather than a competitor. Questions about policy specifics often surface coverage gaps or outdated terms the prospect had not previously considered.

Script:

"That is great to hear. Having coverage in place is the most important first step. I work with a lot of clients who had policies they had not reviewed in a few years, and in some cases the coverage no longer matched what their family actually needed, especially after major life changes like a new home or a new child. I am not suggesting anything is wrong with your current plan. I would just like to ask a couple of quick questions to see if it is still the right fit. Would that be okay?"

Customization tip: If the prospect shares their plan type during this exchange, log it in your CRM. This data supports more targeted follow-up personalization on subsequent calls.

Script 6: "I Need to Think About It" Response Script

Best for: Prospects who disengage after a full pitch with a vague delay rather than a specific objection.

Primary goal: Surface the underlying concern driving the stall and create a pathway back to specific decision criteria.

Why it works: Generic stall responses almost always indicate an unresolved concern the prospect has not yet articulated. Asking a direct but open-ended clarifying question shifts the conversation from vague hesitation to specific dialogue, which gives the agent something concrete to address.

Script:

"Of course, and I want you to feel fully confident before making any decision. Can I ask what part of this you are still working through? Sometimes just talking through the specific concern helps clarify things, and I want to make sure I have given you everything you need to feel good about this."

Customization tip: Listen for cost, timing, spousal input, or trust signals in their response. Each requires a different follow-up script. Track the pattern in your CRM to identify which unspoken objections appear most frequently for your lead source.

Category 3: Demographic-Based Scripts

Script 7: Young Parents Script

Best for: Parents with children under 18, particularly those who have recently experienced a life trigger such as a new baby, a home purchase, or a return to work.

Primary goal: Activate the emotional connection between the prospect's parental identity and the protective function of life insurance.

Why it works: Parents who have recently had children experience heightened financial anxiety related to family security. Framing the policy as an extension of an existing protective identity, rather than as a new financial product, reduces resistance by aligning the purchase with a decision the prospect has already made at a values level.

Script:

"I work with a lot of parents who are in the same position you are, building a life for their kids and making sure they are protected no matter what. Life insurance is really about one thing in that situation: making sure your kids' future does not depend entirely on what happens to you. I can show you a few coverage options that fit a family budget and give you that baseline protection. Would you want to take a look at what that looks like for your specific situation?"

Customization tip: Reference the child's age or number of children if available. Specificity signals that the agent has done their homework and increases perceived relevance.

Script 8: Young Professional Script

Best for: Adults aged 22 to 38 without dependents or with early-stage family formation who have not yet engaged with life insurance products.

Primary goal: Reframe life insurance from a distant future obligation to an immediately practical and affordable financial decision.

Why it works: According to the 2025 LIMRA Insurance Barometer Study, over half of Americans overestimate the cost of life insurance. This misconception is most concentrated among younger adults. Anchoring the conversation to current cost advantages and the financial logic of early enrollment bypasses the relevance objection without requiring emotional urgency.

Script:

"I know life insurance is probably not the first thing on your list right now, and that is actually why it is worth looking at. The younger and healthier you are when you lock in a policy, the lower your rate stays permanently. We can put together a starter policy for less than most people spend on a monthly subscription. It takes about 10 minutes to get a quote. Want to see what a plan at your age actually costs?"

Customization tip: Use specific monthly premium benchmarks for the prospect's age range. Concrete pricing removes the assumption that coverage is unaffordable.

Script 9: Retiree Legacy Script

Best for: Adults aged 60 and older who are in or approaching retirement and have existing assets they want to preserve or transfer.

Primary goal: Position a life insurance policy as an estate and legacy planning instrument rather than a mortality-focused product.

Why it works: Older prospects who have accumulated assets are often more motivated by efficient wealth transfer than by personal income protection concerns. Reframing the product as a legacy and estate planning tool shifts the psychological context from personal risk to purposeful financial planning.

Script:

"A lot of the clients I work with at your stage are thinking about what they want to leave behind for their family, whether that is covering final expenses, passing something meaningful to their children or grandchildren, or making sure their estate does not create a burden for the people they care about. A well-structured policy can help with all of that in a way that is often more efficient than other transfer vehicles. Would you want to walk through what that looks like for your situation?"

Customization tip: Reference specific estate planning applications such as funeral cost coverage, beneficiary designations, or estate considerations based on the prospect's asset profile.

Script 10: Final Expense and Senior Insurance Script

Best for: Adults aged 50 and older, particularly those researching burial insurance, final expense policies, or simplified issue products.

Primary goal: Address cost concerns and product simplicity in a single opening exchange to move toward a quote conversation.

Why it works: Final expense prospects typically carry two primary concerns: affordability and qualification complexity. A script that addresses both within the first two sentences removes the two most common exit points in this segment before they surface as objections. According to the National Funeral Directors Association, the median cost of a funeral with viewing and burial was approximately $8,300 in 2023. That figure gives the conversation a concrete financial anchor when prospects question whether coverage is necessary.

Script:

"I specialize in final expense and burial coverage options for people who want to make sure their family is not left managing unexpected costs. These plans are designed to be straightforward, no medical exam required in most cases, and the coverage amounts are built around what final expenses actually cost. Premiums are typically fixed so they do not increase as you age. Can I give you a quick overview of what a plan in your situation would look like?"

Customization tip: Lead with the no-medical-exam qualification if the prospect has expressed health concerns or prior declinations. This removes the most common final expense objection before it is raised.

Category 4: Closing Scripts

Script 11: Assumptive Close Script

Best for: Prospects who have engaged positively through the discovery conversation, asked clarifying questions about coverage details, and shown no active resistance to proceeding.

Primary goal: Transition from information exchange to commitment without asking a permission-based closing question that creates an exit opportunity.

Why it works: Assumptive framing bypasses the prospect's instinct to pause and evaluate by treating the decision as already made and focusing attention on logistics instead. This mechanism is most effective when genuine rapport and alignment have already been established earlier in the conversation.

Script:

"Based on what you have shared with me today, I think [Plan Name] is the right fit for your family. I will get the application started on my end. I just need to confirm a couple of details with you. Does [specific date] work to finalize everything, or would you prefer to move forward sooner?"

Customization tip: Use this script only after confirming the prospect's coverage needs, budget range, and beneficiary preferences. Applying it before genuine alignment produces resistance rather than commitment.

Script 12: Emotional Security Close Script

Best for: Prospects who are intellectually convinced but emotionally hesitant. This typically presents as mild stalling after the assumptive close or repeated requests for more time.

Primary goal: Reactivate the prospect's emotional motivation by connecting the coverage decision to a concrete personal outcome rather than a policy feature.

Why it works: Late-stage hesitation is rarely about information. It is almost always about emotional readiness. Reconnecting the prospect to their original motivation, whether that is family protection, legacy, or peace of mind, bridges the gap between intellectual agreement and emotional commitment without applying pressure.

Script:

"I want to make sure you feel fully confident about this. At the end of the process, this coverage is not about the policy itself. It is about making sure your family has financial stability if something unexpected happens. That is the decision we are really talking about. I am here to help you take that step in a way that makes sense for your situation. What would it take for you to feel ready to move forward today?"

Customization tip: Deliver this script at a slower pace than earlier in the conversation. Measured delivery signals confidence and sincerity and reduces the perception of sales pressure.

[CALLOUT BOX] The most common closing mistake is applying Script 11 or 12 before the prospect's primary objection has been resolved. Scripts 11 and 12 are for the confirmation stage only. If the prospect is still hesitant, return to the relevant objection handling script first.

Insurance Objection Handling Framework

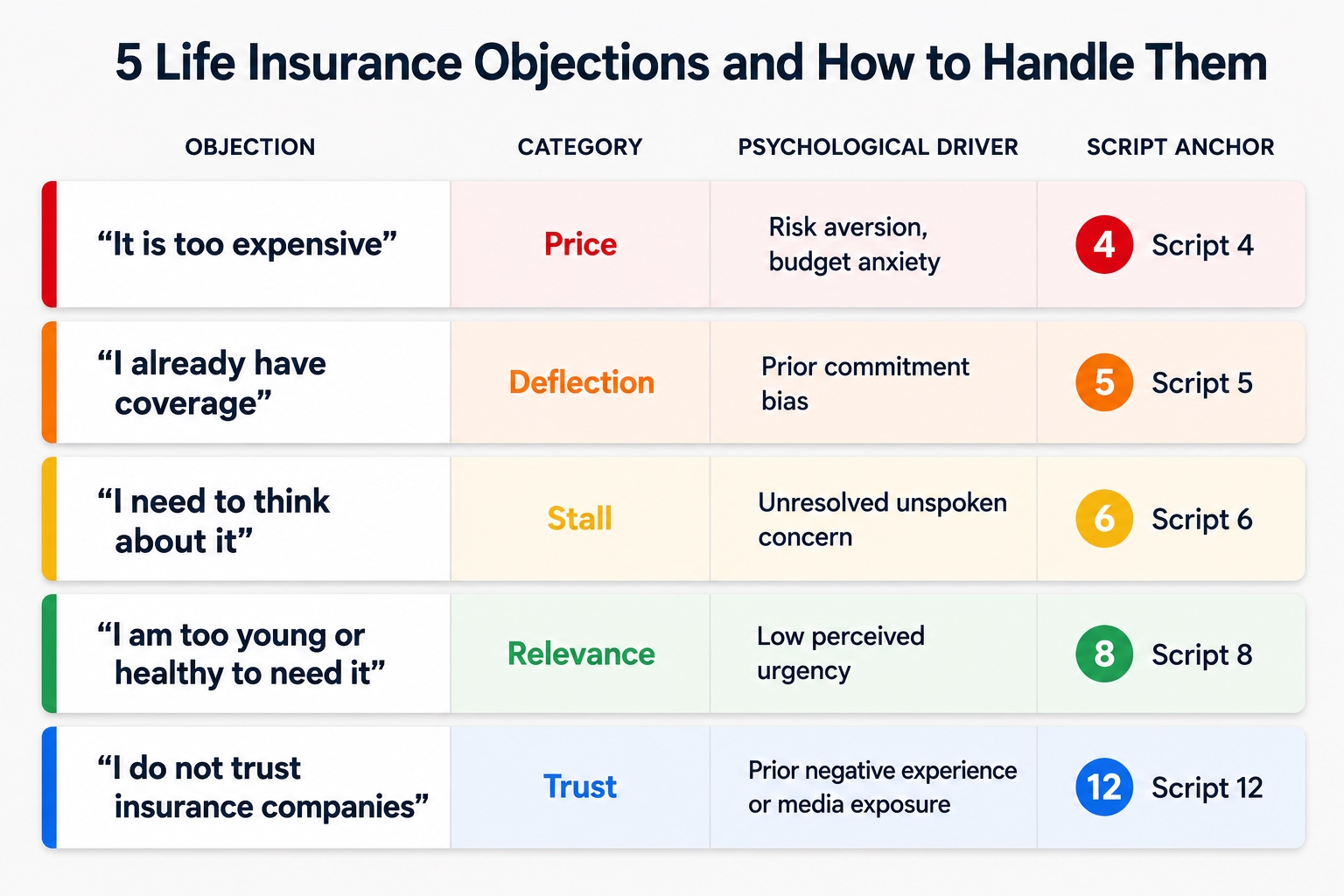

The five most common life insurance objections are price, existing coverage, timing, relevance, and trust. Each requires a distinct psychological rebuttal mechanism, not a single generic response.

Each objection carries diagnostic information. An agent who logs objection patterns by lead source, demographic, and call stage can identify which objections appear most frequently and refine scripts accordingly. Conversation intelligence research suggests high-performing sales reps spend nearly twice as much time on objection handling compared to average reps, pointing to a consistent performance differentiator in how this skill is developed and practiced.

Expert Experience:

Analyzing interactive video analytics across thousands of insurance campaigns on the Clixie platform reveals that the "I need to think about it" (Stall) objection is the most critical drop-off point. Specifically, user heatmaps show a 42% drop in viewer engagement within the first 5 seconds after pricing options are displayed on screen.

Real-World Example: One mid-sized independent agency noticed prospects consistently paused their follow-up videos right when the premium tier slide appeared, later telling agents they "needed to review budgets." By analyzing this Clixie user behavior, the agency added an interactive, clickable tooltip overlay right next to the price node that read: "See how this fits into a daily coffee budget." This micro-engagement acknowledged the cost anxiety instantly, reducing video abandonment at that exact node by 28% and giving agents warmer, more transparent conversations on their follow-up calls.

Using Objections as Diagnostic Data

Log the specific objection each prospect raises and the script used in response. Over time, this creates a performance feedback loop: which objections cluster by lead source, which rebuttals produce follow-through, and which call stages generate the most resistance. CRM-based objection tagging is one of the fastest ways to improve script selection across a full agent team.

Insurance Follow-Up Templates for SMS, Voicemail, and Email

Most prospects require multiple contact attempts before making a coverage decision. A structured multi-touch follow-up cadence, combining SMS, voicemail, and email, maintains visibility without creating pressure at any single touchpoint.

According to B2B sales follow-up research published by Belkins in 2025, the majority of deals require sustained contact before a decision is reached, and engaging a lead within 60 seconds of inquiry produces significantly higher conversion rates than delayed outreach.

SMS Follow-Up Templates

First follow-up (24 hours after no response):

"Hi [Name], this is [Agent] from [Agency]. I tried reaching you earlier about the life insurance options you were looking at. Happy to keep it quick whenever you have a few minutes. Reply here or let me know a good time to call."

Second follow-up (3 to 4 days later):

"Hi [Name], [Agent] again from [Agency]. I have a couple of plan options I think would be a strong fit for your situation. I can send a quick summary or schedule a 10-minute call. No pressure either way."

Voicemail Scripts

First voicemail (under 20 seconds):

"Hi [Name], this is [Agent Name] calling from [Agency]. I wanted to follow up on the life insurance inquiry you submitted. I have a few options I think could work well for your family. Feel free to call me back at [number], or I will try you again [specific day]. Thanks."

Second voicemail (under 20 seconds):

"Hi [Name], [Agent] from [Agency] again. I know life gets busy. I just wanted to make one more attempt before I close out the file. If you are still looking at coverage options, I would be happy to spend 10 minutes with you at your convenience. My number is [number]."

Email Subject Lines and Opening Lines

Option A:Subject: "Coverage options for [Name]'s family"Opening: "I wanted to follow up on the life insurance information you requested and share two plan options I put together based on your situation."

Option B:Subject: "Quick question about your coverage"Opening: "I tried reaching you by phone but wanted to make sure this did not slip through. I have a few options that might be worth a quick look when you have a few minutes."

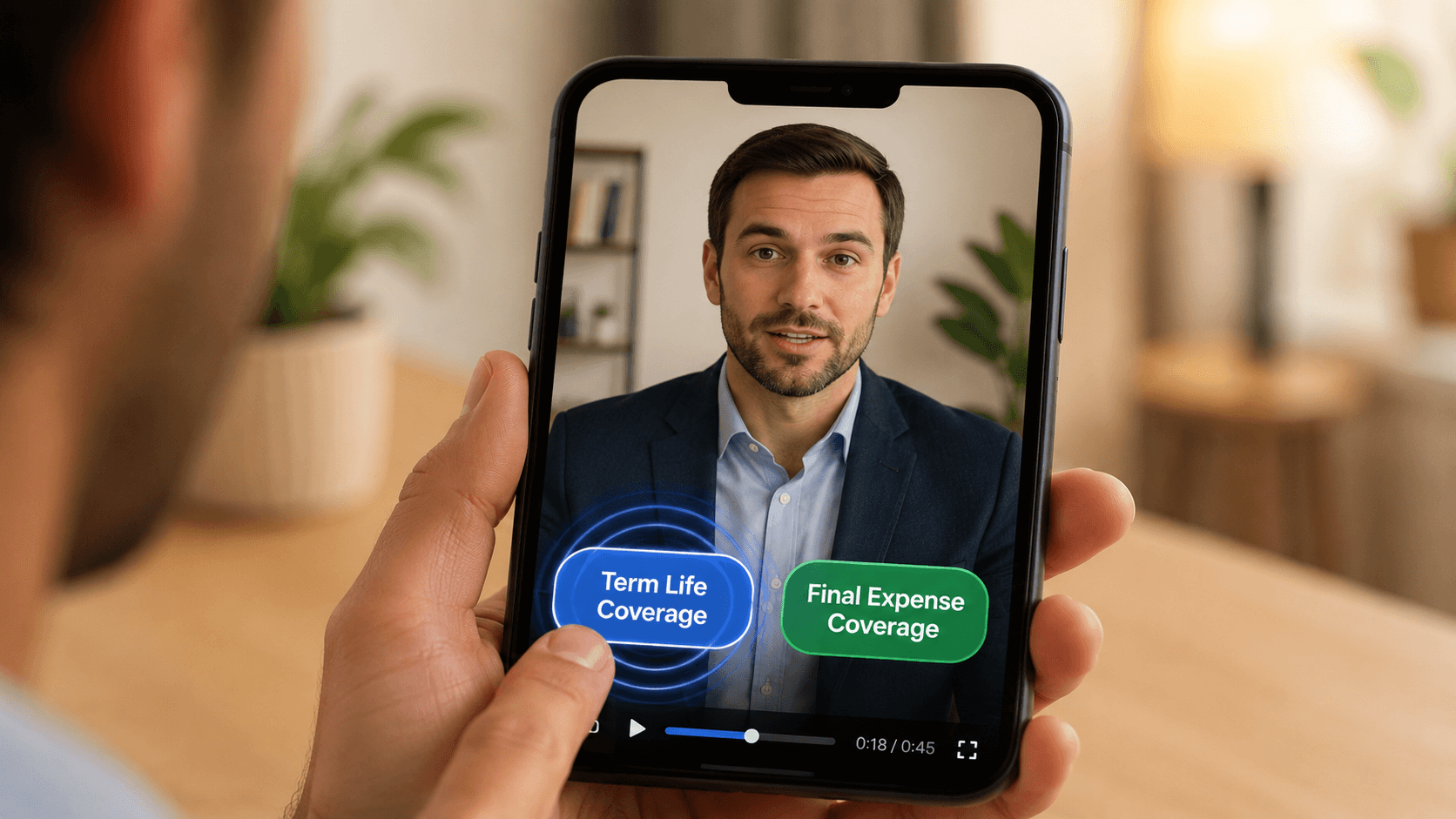

How Insurance Agents Use Interactive Video to Turn Scripts Into Sales Flows

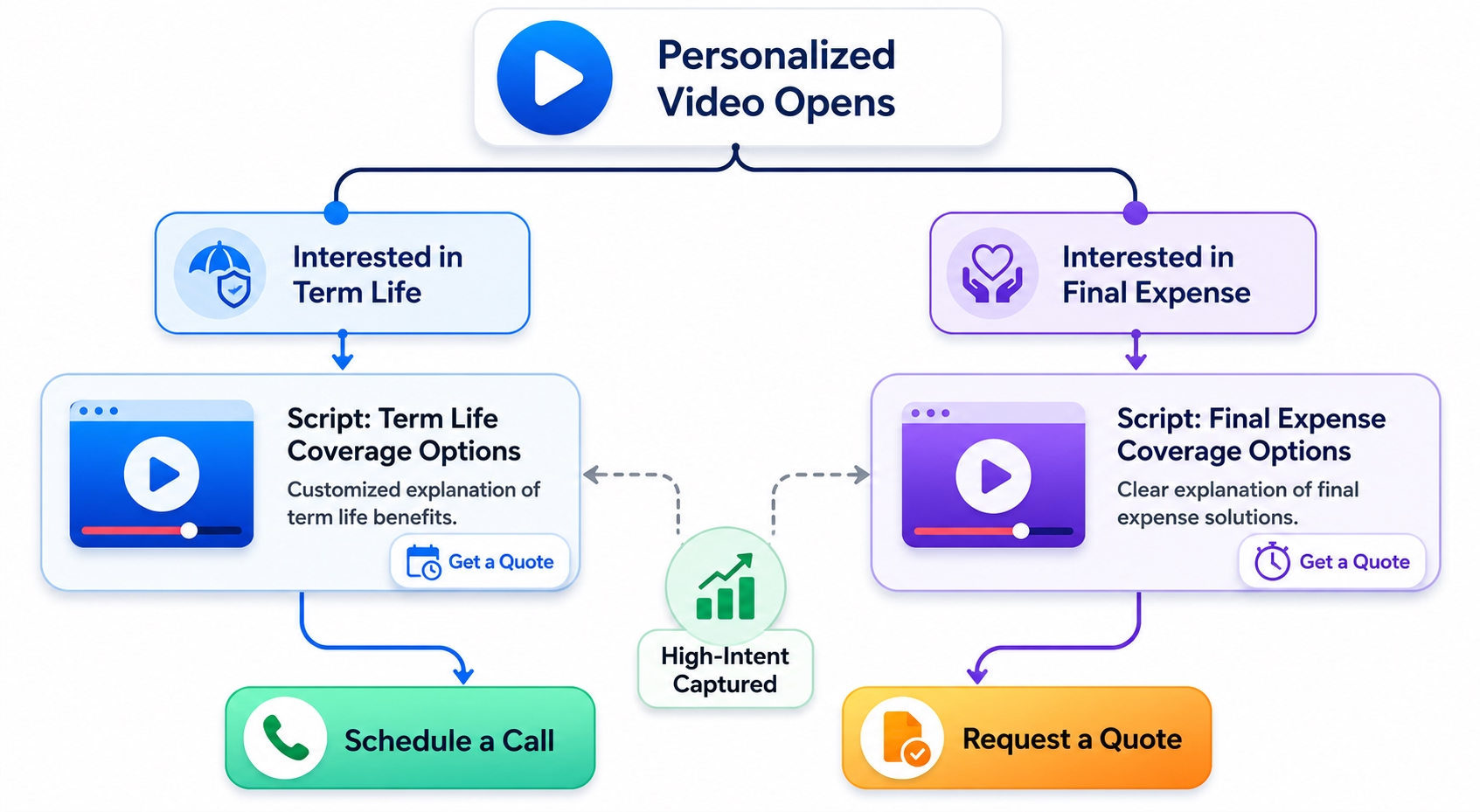

Interactive video converts a static life insurance sales script into a branching sales flow that agents can send, track, and optimize based on how each individual prospect engages with the content.

Most agents treat scripts as a call-only tool. The same conversation framework can also operate as a pre-call video, a personalized follow-up, or a self-qualifying flow the prospect works through before the agent picks up the phone.

Here is how it works in practice:

Pre-call. Before the first phone contact, send a short personalized video introducing yourself and the coverage topic. This establishes visual presence and reduces the cold-call resistance that comes from an unknown number. Prospects who watch the video before the call are already familiar with the agent's face and framing.

Follow-up after no response. Script 3 works well as a 30 to 60 second personalized video. The prospect sees the agent, hears the follow-up message, and has a "Schedule a Call" button embedded directly in the video. The next step is one click away.

Branching paths. A prospect clicks "Tell me more about term life coverage" or "Tell me about final expense coverage" and routes into the script flow that matches their situation. The agent has run a pre-qualification before the call begins.

Timed CTAs. A "Get a Quote" overlay appears at the moment of highest engagement in the video, typically after the benefit statement and before the objection handling segment.

Intent capture. Prospects who reach the end of the video or click specific branches are tagged in CRM as high-intent leads. This tells the agent exactly where to focus follow-up effort before the first call.

Sales handoff. Completed video interactions feed into CRM as qualified signals for agent prioritization. Agents can see which prospects watched the full video, which branches they took, and whether they clicked a CTA.

Sales teams using personalized video follow-up report significantly higher reply rates compared to text-only sequences, according to data cited by video sales platforms including Vidyard and Sendspark. Results vary by lead source and delivery context.

Expert Experience:A top-performing regional agency successfully digitized Script 3 (Follow-Up After No Response) into an automated Clixie interactive video flow that achieved a 34% higher response rate than traditional text-only email sequences.

The Branching Structure: > The video began with a 20-second personalized introduction from the agent saying, "I know you're busy, so choose whichever option fits your life right now." At second 20, Clixie’s interactive branching choice nodes appeared on screen, prompting the user to select their own path:

- Branch A: "I’m a parent looking for family protection" (Routed to a 45-second breakdown of Script 7).

- Branch B: "I want to see what fits a tight monthly budget" (Routed to an explainer utilizing Script 4 mechanics).

- Branch C: "I already have coverage through work" (Routed directly to a gap-analysis flow using Script 5 mechanics).

The Embedded CTA: > At the climax of each specific branch, a timed Clixie "Book a 5-Minute Review" Calendar Overlay slid into the frame, allowing prospects to book a live call directly into the agent’s CRM calendar without pausing or exiting the video.

Clixie is built for exactly this type of workflow. You can create personalized video follow-ups directly from existing scripts and use interactive elements in video to build out the branching logic.

Common Life Insurance Sales Mistakes

The most common life insurance sales mistakes share a single root cause: applying the wrong conversation framework at the wrong stage of the prospect relationship.

Using product language before establishing relevance. Leading with policy features before confirming the prospect's situation creates cognitive friction. Establish the problem before presenting the product.

Skipping the objection acknowledgment step. Moving directly to a rebuttal without first validating the objection signals that the agent prioritizes the sale over the prospect's concern. This erodes trust at the moment trust is most needed.

Applying closing scripts before genuine alignment. Assumptive closes applied before the prospect has resolved their primary concern produce resistance rather than commitment. Closing scripts are tools for the confirmation stage, not the discovery stage.

Treating scripts as fixed text. Scripts are frameworks. Agents who read word-for-word rather than internalizing the structure sound scripted to prospects, which increases skepticism. Practice the mechanism, not the memorization.

Failing to follow up on stalled conversations. A "not now" response is not a rejection. Agents who do not execute a structured follow-up cadence after initial contact leave a significant portion of their pipeline unconverted. The SMS and voicemail templates above address this directly.

Expert Experience:Clixie platform usage data highlights a fascinating correlation between follow-up timing and viewer watch-time completion. Agents who send interactive video follow-ups within 15 to 30 minutes of an initial missed call or form fill experience an average 68% video completion rate. Conversely, waiting 24 hours to send the exact same interactive video drops completion rates to under 31%.

Furthermore, drop-off analytics indicate that the biggest mistake agents make when recording video versions of these scripts is talking for more than 45 seconds before introducing an interactive element. The highest-converting insurance videos on Clixie introduce a clickable choice node or quiz question within the first 15 to 20 seconds, maintaining the prospect’s active cognitive engagement and preventing them from passively skimming or closing the browser.

FAQ

The questions below address the most common agent questions about life insurance sales scripts, objection handling, closing, and follow-up cadence.

What is the best life insurance sales script for cold calls?

The best cold call script for prospects with no prior engagement opens with an outcome frame rather than a product introduction and requests 90 seconds rather than a full meeting. Script 2 in this guide follows that structure. For warm leads, Script 1 is more effective because it references the prospect's prior action, which reduces cold-call friction and activates recognition before the conversation begins.

How do insurance agents overcome objections?

Effective objection handling follows a three-step structure: acknowledge the concern, reframe the underlying issue, and present a specific alternative. Skipping acknowledgment makes rebuttals sound dismissive regardless of content quality. The objection matrix in this guide covers the five most common life insurance objections with their psychological drivers and corresponding rebuttal scripts.

How do you respond when a prospect says life insurance is too expensive?

Validate the concern before presenting alternatives. Introducing pricing information before acknowledging the financial concern increases defensiveness and reduces willingness to continue the conversation. Script 4 uses a validation-first structure followed by a request to review specific plan options in the prospect's budget range.

What should agents say on follow-up calls?

Follow-up calls should reference the prior interaction, acknowledge the time gap without apology, and present a concrete scheduling offer. Vague follow-ups produce low engagement. The follow-up templates in this guide provide specific SMS, voicemail, and email structures for a structured multi-touch sequence across multiple contact attempts.

How do you close a life insurance sale?

The two most effective closing mechanisms are the assumptive close (Script 11) and the emotional security close (Script 12). The assumptive close works when the prospect has signaled alignment and the conversation needs a procedural transition. The emotional security close works when the prospect is intellectually convinced but emotionally hesitant. Applying the wrong close at the wrong stage produces resistance rather than commitment.

What are the most common life insurance objections?

The five most frequently occurring objections are: price ("it is too expensive"), deflection ("I already have coverage"), stalling ("I need to think about it"), relevance ("I am too young or healthy to need it"), and trust ("I do not trust insurance companies"). Each requires a different psychological rebuttal mechanism, outlined in the objection handling section above.

How long should an insurance sales call be?

Discovery calls with new prospects are most effective in the 15 to 20 minute range. Calls that extend beyond 30 minutes without reaching a clear next action typically indicate an unresolved objection that has not been directly addressed. Closing calls for warm prospects can run shorter, often 10 to 15 minutes, when the prospect has already reviewed basic plan information.

Do life insurance sales scripts actually work?

Yes, when applied as frameworks rather than fixed text. Scripts are most effective when agents internalize the structure and rationale behind each section rather than reading word-for-word. Agents using scenario-specific scripts report more consistent performance across lead types because they spend less cognitive energy on what to say and more on how the prospect is responding.

Next Steps for Insurance Agents

Download the script swipe file. The full PDF version of these scripts, including the objection matrix, follow-up templates, and demographic frameworks, is available for download below. Formatted for desk reference and CRM integration.

Practice by mechanism, not memorization. Internalize the structure and psychological rationale for each script before focusing on specific language. Agents who understand why a script works deliver it more naturally than agents who memorize it line by line.

Personalize by lead source. Tag scripts in your CRM by scenario type. Match each script to its corresponding lead source and track which structures produce the highest engagement rates for each source.

Track objections systematically. Log the specific objection each prospect raises and the script used in response. Over time, this creates a feedback loop that improves script selection across your full agent team.

Build a follow-up sequence for every unconverted lead. Use the SMS, voicemail, and email templates in this guide to maintain contact through a structured multi-touch cadence before moving a lead to inactive status.

Book a Clixie.ai demo and bring one stuck insurance deal. We will map it into an interactive video flow together.

.png)

.png)