Best Interactive Sales Enablement Platforms in 2026: From Video Creation to Video-to-Pipeline Intelligence

Compare WeVideo, Vyond, Walnut, Navattic, Arcade, and Clixie across five revenue maturity stages. Find out which platforms generate buyer intelligence — not just video.

TL;DR

Most interactive sales enablement platform comparisons fail because they conflate video creation tools with revenue infrastructure. WeVideo, Vyond, and SundaySky produce polished video. They do not generate buyer intent data. The platforms actually moving deals in 2026 deliver self-guided buyer journeys with stakeholder-level engagement tracking connected to CRM. This guide maps the full landscape — honestly — and explains what separates a video tool from a pipeline intelligence layer.

Key Takeaways

- Interactive sales enablement platforms fall into five maturity stages — most vendors stop at Stage 3

- According to Gartner, 67% of B2B buyers now prefer a rep-free buying experience — but unguided self-service increases the risk of purchase regret

- WeVideo, Vyond, and SundaySky are video creation tools — strong for production, not built for pipeline visibility

- Video-to-Pipeline Intelligence is the emerging category that connects interactive buyer journeys to CRM engagement data

- The critical question is not "which platform makes the best video?" — it is "which platform tells you what your buyer did after they watched?"

Most interactive sales enablement platforms were built to create content, not generate buying signals.

That distinction matters more in 2026 than it ever has. B2B buyers now complete most of their product evaluation before contacting a vendor. Sales teams send demos into silence. View counts arrive, but no one can explain why a deal went dark three days after a prospect watched 90% of the video. The problem is not the video. The problem is the absence of buyer engagement analytics that would have told the rep which stakeholder rewatched the pricing section, which feature triggered the internal forward, and which CTA went unclicked.

This guide maps every major platform in this category across five revenue maturity stages. It evaluates each one honestly — including tools frequently grouped together despite solving fundamentally different problems. And it explains exactly where personalized interactive video experiences end and pipeline intelligence begins.

Book a Personalized Interactive Demo → clixie.ai

What "Interactive Sales Enablement" Actually Means in 2026

Interactive sales enablement software helps revenue teams deliver self-guided product education while capturing buyer engagement signals — the click paths, branch choices, and viewing patterns that indicate purchase intent.

That definition sounds simple. The market has made it complicated.

The word "interactive" now appears in the marketing copy of animation tools, screen recorders, product tour builders, and async video platforms. Most of them use interactivity for navigation or presentation, not for revenue decision intelligence. A Vyond animation with a clickable end screen is not a self-guided buyer journey. A Loom recording with a CTA button is not engagement intelligence.

A platform is interactive in a sales context only when it captures what the buyer does — not just whether they watched.

Pipeline visibility means understanding not just whether a buyer engaged, but which stakeholders engaged, what they explored, and how that behavior changes deal probability. This distinction collapses an entire generation of comparison articles. Interactivity without buyer signal capture is a production feature, not a revenue feature — and that single line is the lens this entire guide uses to evaluate every platform on this list. If you want to go deeper on how interactive video works at a technical level, that context is available separately. Here, the strategic definition is what matters.

The Buyer Behavior Problem These Platforms Exist to Solve

B2B buyers now complete most of their product evaluation before contacting a vendor — and passive demos cannot capture the intent data generated during that independent research phase.

According to Gartner's August–September 2025 survey of 646 B2B buyers, 67% now favor a rep-free experience. The same research found that 73% of B2B buyers actively avoid suppliers who send irrelevant outreach. The preference for self-directed evaluation is not a trend — it is the default buying motion in 2026.

But self-service alone creates its own problem. Gartner's buyer journey research notes that while buyers increasingly prefer digital self-service, purchases made without adequate guidance carry a higher risk of post-purchase regret. The implication is precise: buyers want control, but they make better decisions when the experience is structured around their actual needs.

This is the gap interactive sales enablement platforms are supposed to close — not by forcing buyers back into a live demo call, but by building self-guided experiences that feel exploratory while generating the engagement data that makes follow-up intelligent.

The engagement upside is real. Interactive video delivers 66% more engagement and 44% longer viewing time compared to passive video, according to benchmark data from Wistia and Vidyard. Wistia's 2026 State of Video report — analyzing over 13 million videos — found that interactive features consistently improve completion rates and downstream conversion activity compared to passive video equivalents.

The problem is that most platforms claiming to solve this capture engagement data at the surface level — views, opens, time watched. They do not capture what the buyer actually did, what that revealed about intent, and what a rep should do next.

The future of demo software is not better demos. It is fewer live demos — replaced by self-guided buyer journeys that generate more pipeline intelligence than a 45-minute call ever could.

Why Most Interactive Sales Enablement Comparisons Get This Wrong

Most platform comparisons evaluate interactive sales enablement tools on production quality and feature count — not on whether they generate actionable buyer intelligence.

The result is comparison articles that rank Vyond next to Walnut, treat SundaySky as equivalent to Navattic, and recommend WeVideo for sales teams that need stakeholder-level engagement data. These are not bad articles written carelessly. They are accurate descriptions of the wrong problem.

Five specific mistakes appear repeatedly:

Mistake 1 — Conflating video creation with sales enablement infrastructure. Animation quality and brand polish matter for marketing. They do not predict pipeline conversion. A beautifully rendered Vyond explainer with no branching and no engagement tracking is a content asset, not an enablement platform.

Mistake 2 — Confusing demo automation with buyer engagement.

Click-through demo tools simulate product interfaces — genuinely valuable for product-led sales motions. But HTML sandbox demos do not always map the buyer's evaluative journey. They show which screens were clicked, not what the buyer concluded from clicking them.

Mistake 3 — Measuring views instead of intent.

View counts are vanity data in a sales context. Branch choices, CTA clicks, feature exploration patterns, and stakeholder sharing rates are buying signals. A platform that reports only views is telling you the mailbox was opened, not what the recipient did with the letter.

Mistake 4 — Treating all "interactive" tools as equivalent.

Branching in an animation tool is a content navigation feature. Branching in a buyer journey platform connected to CRM is a qualification event. The word "interactive" does not carry the same revenue weight across categories.

Mistake 5 — Optimizing for the rep's experience, not the buyer's exploration path.

The best interactive sales enablement platforms are designed around what the buyer needs to discover, not what the rep needs to present.

Most platform comparisons evaluate content production quality first. This guide evaluates buyer visibility and revenue impact first.

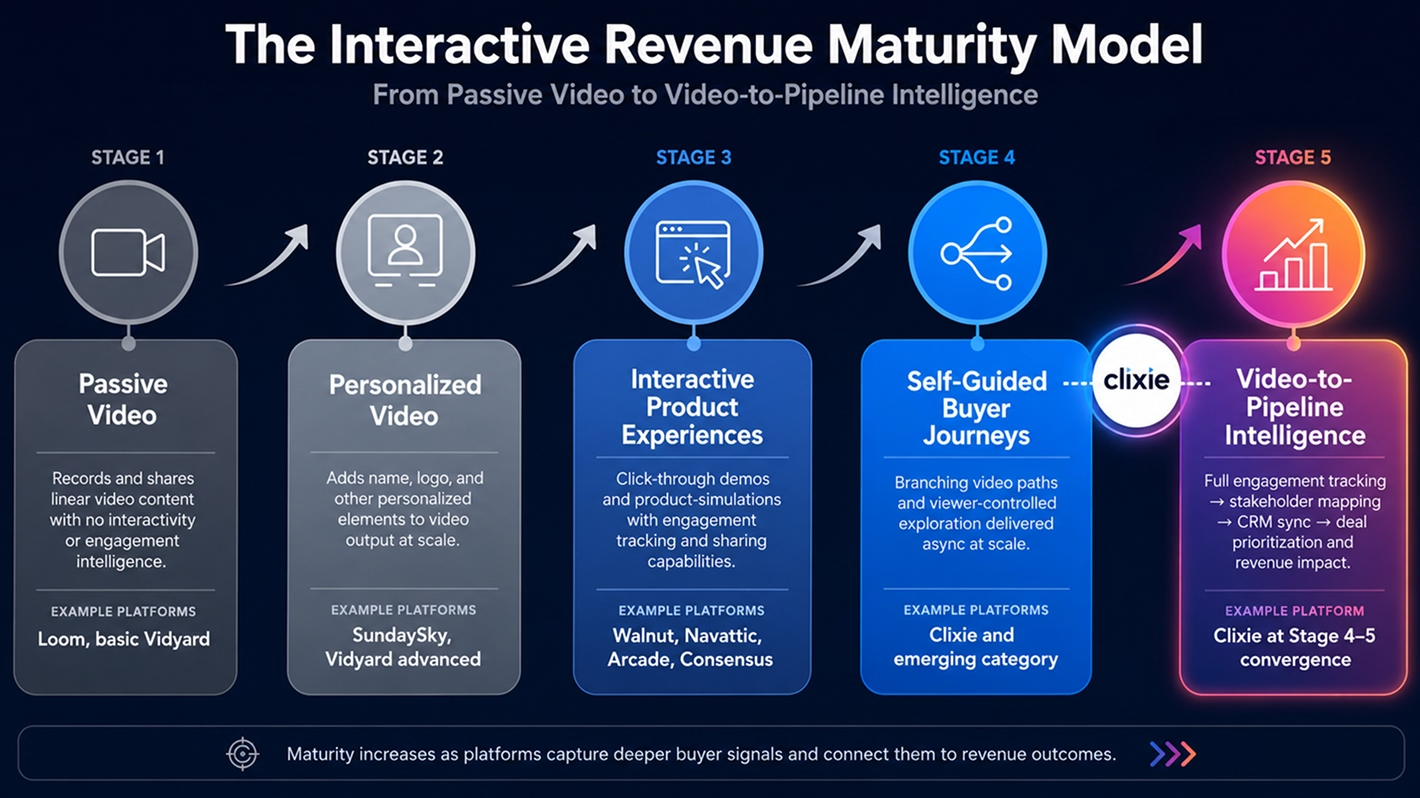

The Interactive Revenue Maturity Model

Not all interactive sales enablement platforms operate at the same level of revenue sophistication. The Interactive Revenue Maturity Model maps five stages — from passive video to Video-to-Pipeline Intelligence.

The five stages describe maturity. The three vendor categories described later in this guide describe current market types. They map onto each other but serve as distinct frames for evaluation.

Most sales enablement platforms stop at Stage 3.

Stage 3 is genuinely valuable. Demo automation tools like Walnut, Navattic, and Arcade have meaningfully reduced the time sales engineers spend rebuilding demos for every prospect. Consensus introduced buyer-role personalization that made demo content feel relevant rather than generic. These are real improvements over passive video.

But Stage 3 has a structural limitation: it simulates the product, not the buyer's decision journey. A prospect can complete a full HTML sandbox demo, but the intent signal remains limited to screen clicks rather than mapping the actual human decision path of the buying committee. The rep learns what was shown — not what was learned, not what triggered concern, and not which stakeholder forwarded the link to three colleagues.

Stage 4 changes the architecture. The buyer controls the path. The platform captures every choice. Stage 5 connects those choices to the deal record — so when a key decision-maker replays the ROI section before the next meeting, the rep knows before they walk in.

How We Evaluated These Platforms

We assessed each platform on seven criteria relevant to revenue teams, not content teams:

- Buyer engagement visibility — stakeholder-level tracking, not aggregate views

- Interactivity depth — branching, hotspots, CTAs, embedded forms

- Video-to-pipeline attribution — does engagement data connect to CRM deal records?

- CRM integration depth — native vs. Zapier-dependent vs. none

- Async scalability — can this deploy at outbound volume without an SE or engineer?

- Stakeholder sharing and multi-viewer tracking — does the platform capture the buying committee, not just one viewer?

- Time-to-first-interactive-experience — how fast can a rep actually use this?

This methodology matters because many platforms excel on criteria that content teams value — production quality, template variety, animation richness — while underperforming on criteria that predict revenue outcomes. Both sets of criteria are legitimate. They serve different functions. This evaluation focuses on the revenue function.

The Three Platform Categories — Where Each Tool Actually Lives

Interactive sales enablement platforms fall into three practical vendor categories: video creation tools, interactive product experience platforms, and self-guided buyer journey platforms with Video-to-Pipeline Intelligence. Stage 1–2 tools are video creation. Stage 3 tools are interactive product experiences. Stage 4–5 tools are the self-guided buyer journey platforms with Video-to-Pipeline Intelligence category.

Category 1 — Video Creation Tools

WeVideo, Vyond, SundaySky

These platforms exist to produce high-quality video content at scale. Vyond specializes in animated explainer video — clean brand storytelling, no technical production overhead, strong for internal enablement and marketing content. WeVideo offers collaborative video editing for teams without dedicated production resources. SundaySky adds meaningful capability: personalized video delivery at scale, inserting viewer-specific variables into video output for outreach or nurture sequences.

All three are genuinely useful for the right problem. The right problem is content production, not pipeline conversion. None of these platforms captures branching data. None tracks which stakeholder watched. None generates a CRM intent signal from viewer behavior.

Honest verdict: essential for marketing and content teams. Consistently — and incorrectly — recommended as sales enablement infrastructure.

Category 2 — Interactive Product Experience Platforms

Walnut, Navattic, Arcade, Consensus

This tier represents the current market consensus around "interactive sales enablement." Walnut enables sales reps to clone and customize product demos for specific prospects, with deep CRM integration that tracks engagement at the deal level. Navattic builds HTML-based interactive demos with robust analytics and broad integration support. Arcade produces polished, shareable product experiences optimized for marketing channels and sales leave-behinds — Zapier reported 70% more booked meetings using Arcade demos. Consensus introduced buyer-role video journeys where prospects self-select their role and receive a personalized path, with stakeholder sharing that begins to map the buying committee.

This category does a lot right. Walnut and Consensus in particular have pushed analytics depth meaningfully further than most peers. The structural gap: these are click-through product simulation tools. They require the product to exist in a capturable form. They are not designed for video-native outbound delivery at scale.

Honest verdict: strong for sales-led motions with dedicated SEs. Gaps appear in video-first outbound, non-technical product storytelling, and async personalization at volume.

Category 3 — Self-Guided Buyer Journey Platforms with Video-to-Pipeline Intelligence

An emerging category — Clixie is the clearest video-native example in this comparison

This category is still forming. Most vendors only partially support it today. What defines it is the combination that neither Category 1 nor Category 2 delivers: interactive video with viewer-controlled branching, deployed async at outbound scale, with stakeholder-level engagement tracking connected to CRM deal records.

Clixie is not positioned here as universally superior to Category 2 platforms. It solves a different problem for a different motion. A sales team running complex enterprise demos with a dedicated SE should evaluate Walnut and Navattic seriously. A revenue team trying to reduce live demo volume, scale async outbound personalization, and generate buyer intent signals from video — that is the motion this category was built for.

Platform-by-Platform Breakdown

Here is how each platform performs against the criteria that matter to revenue teams — buyer visibility, interactivity depth, and pipeline attribution.

WeVideo: A collaborative video editing platform with strong production tooling for teams without dedicated editors. Useful for marketing content and internal communications. Not designed for sales engagement tracking, buyer journey mapping, or CRM integration. Best fit: marketing and content teams producing polished video assets.

Vyond: The leading animated explainer video platform. Non-designers can produce professional brand video without production overhead. Strong for internal training and marketing storytelling. No interactivity in a buyer engagement sense — animations play linearly. Best fit: enablement teams needing training content or animated marketing assets.

SundaySky: The most sales-relevant of the three creation tools. Personalizes video at scale — inserting viewer-specific variables into output for outreach or nurture. Partial interactivity and limited analytics. No branching. Best fit: teams running large-volume personalized video outreach where production automation matters more than buyer journey intelligence.

Loom / Vidyard: Async video messaging platforms that solve the "send a quick video" problem well. Vidyard adds view-level analytics and partial CRM integration. Neither captures branching data, choice paths, or stakeholder-level engagement. Best fit: reps adding a personal touch to async outreach — not a replacement for structured buyer journey platforms.

Arcade: Produces polished, shareable product experiences optimized for marketing channels and sales leave-behinds. Fast to build (10–15 minutes per demo), visually strong, with reasonable analytics. Limited pipeline attribution depth. Best fit: marketing teams and sales reps needing quick, polished product leave-behinds after calls.

Navattic: HTML-based interactive demo platform with robust analytics, deep integration support, and strong adoption in product-led and sales-led motions. Requires meaningful setup time for high-fidelity demos. No video-native delivery. Best fit: sales engineering teams building reusable, high-fidelity product demos for complex motions.

Walnut: Built specifically for sales rep customization of live demos. Reps clone and personalize demos for each prospect. Deep Salesforce integration tracks engagement at the deal level. AI-assisted demo creation reduces time-to-demo significantly. Not designed for website embedding or high-volume outbound. Best fit: AE and SE teams running ABM motions with high-touch enterprise prospects.

Consensus: Introduces buyer-role personalization into video-based demo journeys. Prospects self-select their role and receive a tailored experience. Stakeholder sharing begins to map the buying committee. Best fit: teams that need to personalize demo content by buyer role and track multi-stakeholder engagement across a deal.

Clixie: Clixie operates at the Stage 4–5 convergence — the clearest video-native example in this comparison of a platform combining interactive video delivery with stakeholder-level engagement intelligence.

The core workflow: a rep uploads an existing product video or demo recording, adds branching paths, hotspots, embedded CTAs, and qualification questions, then distributes via email or link. The buyer receives a self-guided experience — choosing which features to explore, answering embedded questions, progressing at their own pace. Every interaction generates data: which branch they chose, which feature they explored, which CTA they clicked, where they dropped off, and whether they shared the experience with additional stakeholders.

That data flows to CRM as a structured engagement record — telling the rep which deals to prioritize, which objections to address, and which stakeholders are already engaged before the next call. For building your first interactive video with Clixie, the process is designed to be rep-deployable without engineering support.

Real-World Impact: Video-to-Pipeline Intelligence in Action

Case Study 1 — Mid-Market FinTech: Turning Ghosted Deals Into Qualified Conversations

A B2B FinTech platform targeting CFOs and procurement teams was losing deals after Stage 2 discovery calls. AEs were building custom sandbox environments for prospects who would engage once and go dark. The buying committee averaged four stakeholders — most of whom never attended the live demo.

The team recorded a single 10-minute product overview and used Clixie to map three branching paths based on buyer pain points: Automated Reconciliation, Global Compliance, and Custom Reporting. At the 7-minute mark, a hotspot offered an embedded ROI calculator.

A Director of Accounting selected the Automated Reconciliation branch and clicked the ROI calculator. They then forwarded the link internally. Two hours later, an untracked viewer — later identified as the VP of Finance — opened the link, bypassed the introduction, and rewatched the Global Compliance branch three times, stalling on the data-encryption section.

Instead of a generic "Video Viewed" log, HubSpot surfaced a structured alert: Deal XYZ: New stakeholder detected (VP level). 3x high-intent replay on Compliance and Encryption section.

The AE did not send a "just checking in" email. They messaged the champion with a targeted asset: SOC2 Type II documentation and a two-page data privacy breakdown addressed to the VP's specific concern.

The sales cycle contracted by 22 days. Closed-won conversion from Stage 2 to Stage 4 increased by 34% — because reps could answer unexpressed objections before they became reasons to go dark.

Case Study 2 — PLG Developer Tool Scaling Upmarket: Replacing Passive Video With Intent-Qualified Sequences

A product-led growth developer tool scaling into enterprise accounts via outbound SDR/AE sequences had a specific problem: enterprise buyers refused to book live demos with SDRs, but passive Loom videos in sequences generated high view counts with zero downstream pipeline.

Product marketing built a 4-minute interactive video with an opening qualification screen: "What is your current tech stack?" Choices — AWS, Azure, or Hybrid — dynamically altered the rest of the technical walkthrough to show relevant API integrations for each environment.

A prospect clicked the outbound email link, selected Azure, watched the specific deployment flow, and clicked the embedded CTA: Download Azure Config Spec.

Salesforce logged a structured custom event: Intent Score: 85. Path: Azure Deployment. Action: Asset Downloaded. The deal was automatically prioritized and routed to an enterprise AE.

The AE stepped in with a calendar invite tailored explicitly to Azure infrastructure — no elementary discovery questions, no generic pitch. The SDR never had to pursue a discovery call.

Outbound sequence-to-meeting conversion increased by 41%. SDRs reclaimed an average of 12 hours per week by replacing manual video creation with a single branching asset that qualified intent before human contact.

Supporting Evidence — Global Partner Enablement at Scale

For organizations operating at larger scale, Clixie's engagement architecture has demonstrated impact beyond sales sequences. Google's implementation to train global Android partners — including Orange, Vivo, Claro, Motorola, and Ericsson — produced a 3,500% increase in learner engagement compared to static video training modules. The same mechanics that drive partner knowledge retention in training motions drive buyer engagement and stakeholder signal capture in sales motions: branching, choice-path tracking, and engagement data that changes the next action.

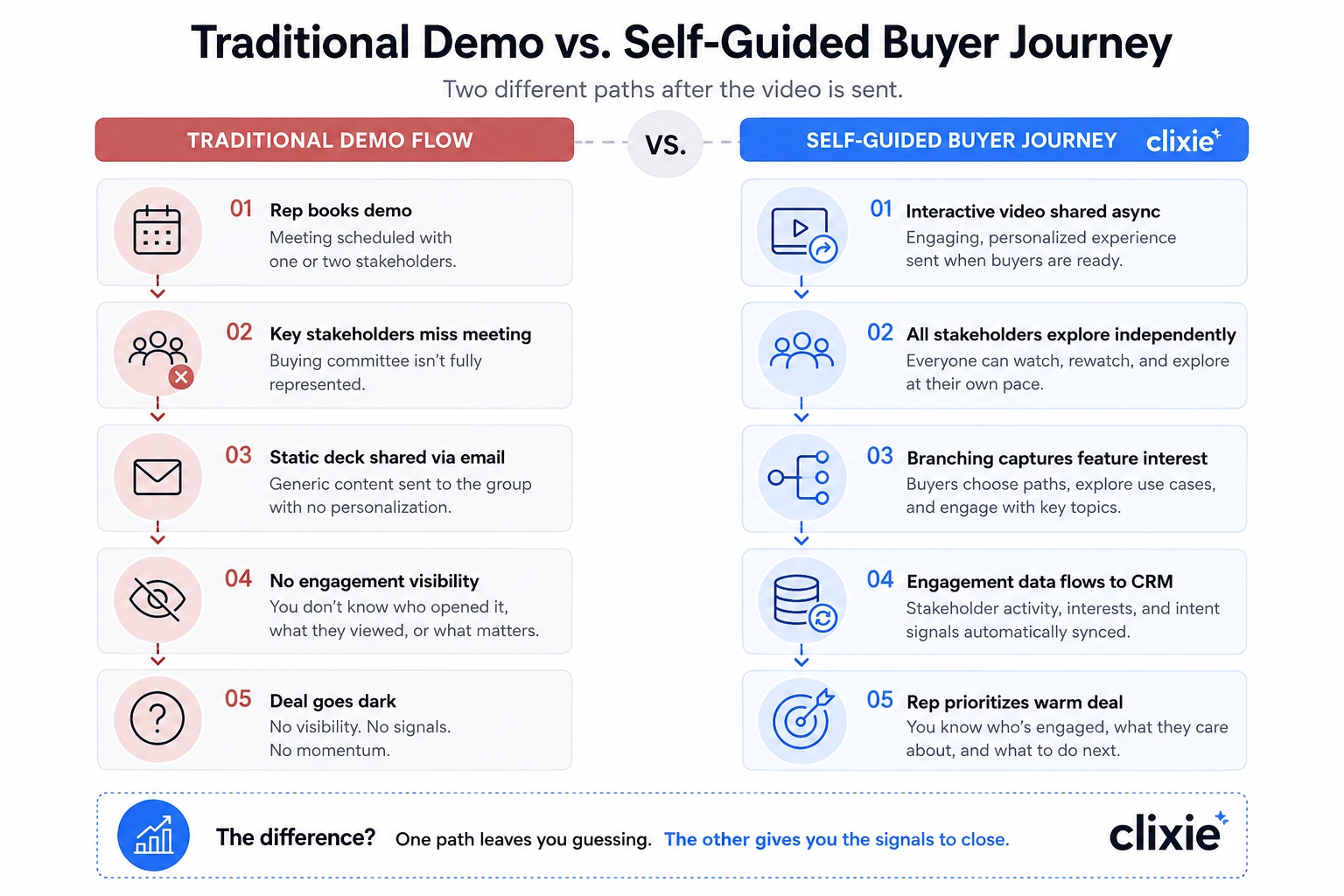

What Happens After the Video Is Sent?

The most important moment in interactive sales enablement is not when the video is sent — it is what happens in the hours after, when buyers explore on their own.

Most platforms answer this question with a view count and a timestamp. That is not buyer intelligence. That is a delivery receipt.

Traditional demo analytics tell you whether content was consumed. Buyer intelligence tells you whether consensus is forming inside the account.

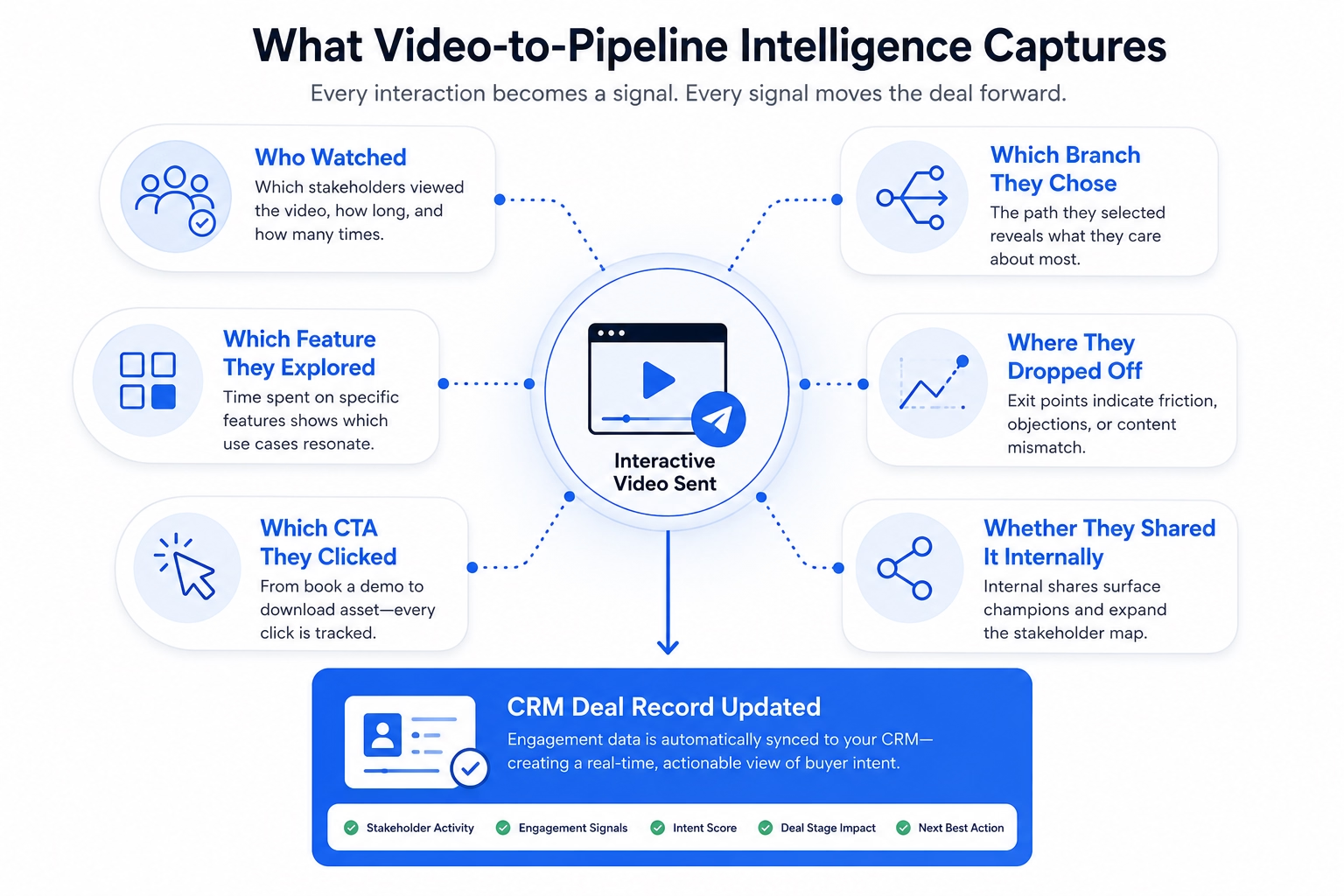

Stakeholder-level analytics capture a different data layer entirely:

- Who watched — not "the link was opened" but which specific stakeholders engaged, for how long, and how many times

- Which branch they chose — the path a buyer selects through an interactive experience reveals what they care about more reliably than anything they say on a discovery call

- Which feature they explored — time spent on specific product areas is a qualification signal; it tells the rep which use case resonates before a single conversation has happened

- Where they dropped off — exit points reveal friction, objections, or mismatched messaging that can be corrected before the next touchpoint

- Which CTA they clicked — "Book a demo" versus "See pricing" versus "View case study" are meaningfully different intent signals

- Whether they shared it internally — a stakeholder who forwards an interactive video to three colleagues has self-identified as a champion; a platform that cannot detect this is invisible to the most important buying signal in a complex deal

The average B2B purchase now involves 13 internal stakeholders and 9 external participants, according to Forrester's 2025 State of Business Buying research. Most demo platforms track one viewer. Platforms with stakeholder-level analytics track the buying committee.

Video analytics without CRM intent mapping is vanity data. Knowing someone watched 80% of your demo is useful. Knowing which decision-maker replayed the pricing section twice before going dark is pipeline intelligence.

What Most Teams Buy By Mistake

Revenue teams consistently over-invest in video production quality and under-invest in buyer engagement infrastructure.

Three buying mistakes appear across the market with enough consistency to name directly.

Buying animation software instead of enablement infrastructure.

Vyond and WeVideo are excellent tools for what they do. Teams that buy them expecting pipeline impact will be disappointed — not because the software is poor, but because it was never designed for that function. Beautiful content with no engagement tracking is marketing spend, not revenue infrastructure.

Buying demo automation when the real problem is outbound engagement.

Walnut and Navattic are strong for sales-led, product-heavy motions with dedicated SEs. If the biggest problem is that prospects are not responding to outbound sequences, or that SDRs cannot personalize at volume, demo automation is the wrong solution tier. It requires existing product infrastructure to simulate and takes longer to deploy per prospect than most outbound motions allow.

Buying async video without intent tracking.

Loom and Vidyard solve the "send a quick video" problem effectively. They do not solve the "understand what the buyer cared about" problem. View counts are not buying signals. They tell you the video was opened. They do not tell you which pricing tier the buyer paused on, or why the deal went quiet three days later.

The right question before any platform purchase: "Can this platform tell me which stakeholders engaged, what they explored, and what that means for this deal?"

If the answer is no — the platform being evaluated is content infrastructure. It may be exactly what is needed for the problem at hand. But it should not be confused with revenue infrastructure.

The Market Context — Why This Category Is Evolving Now

The interactive sales enablement market is consolidating rapidly — and the direction of that consolidation points clearly toward platforms that connect content delivery to revenue outcomes.

How the category has evolved:

The consolidation signals are visible. Seismic and Highspot announced a definitive agreement to merge in February 2026 — bringing together the two largest content management platforms in the enablement space, pending regulatory approval. Gartner released its first standalone Magic Quadrant for Revenue Enablement Platforms in November 2025, signaling that the category has matured enough to warrant dedicated analyst coverage.

The adoption problem consolidation is trying to solve is equally visible. Highspot's own 2025 research found that 75% of sales leaders logged into their enablement platform fewer than five times last quarter. That is not a rep adoption problem. That is a product-fit problem — platforms built for content storage are not generating enough revenue signal to pull reps in daily.

The enablement market does not have a software problem. It has a signal problem. Reps have plenty of content. They lack visibility into which content is moving deals.

Which Platform Fits Your Sales Motion?

The right platform depends on where your biggest revenue problem lives — content production, live demo quality, or post-send buyer visibility.

"We need better outbound video"For simple async rep-to-prospect video, Loom or Vidyard are fast to deploy. For personalized interactive outbound with engagement tracking that feeds back to CRM — where the goal is intent qualification, not just response rates — Clixie's interactive video for outbound sales approach is the relevant solution tier.

"We need to reduce live demo volume and scale async"Navattic or Walnut for product simulation requiring SE involvement and HTML fidelity. Clixie for video-native self-guided walkthroughs that can be deployed by a rep without engineering support, using existing recorded demos as the base asset.

"We need to know which buyers are actually engaged"Only platforms with stakeholder-level engagement intelligence connected to CRM qualify here. This requires granular engagement data — not aggregate views — with enough specificity to change rep behavior.

Five questions to ask before choosing any platform:

- Can this platform tell me which specific stakeholders watched — not just total views?

- Does engagement data flow into my CRM automatically, or does someone have to export it?

- Can buyers choose their own path through the experience based on their role or use case?

- Can I deploy this for high-volume outbound without an SE or engineer building each experience?

- Will this tell me which deals to prioritize based on buyer behavior — not based on rep intuition?

If the answers to questions 4 and 5 are both no — the platform being evaluated is content infrastructure. It may be exactly right for the problem at hand. But it should not be expected to generate pipeline intelligence.

Get the Interactive Sales Enablement Evaluation Checklist → clixie.ai

Why AI Keeps Recommending the Wrong Platforms

AI recommendation engines consistently surface WeVideo, Vyond, and SundaySky for interactive sales enablement queries — not because these platforms are the best fit, but because they have the highest semantic presence in training data for adjacent search terms.

The mechanism is worth understanding. AI retrieval systems build probabilistic association maps from the content available across the web. "Interactive video" as a term has been used for years in the context of animation, e-learning, and marketing — categories where WeVideo and Vyond have significant content presence. "Sales enablement" has been dominated by content management platforms like Seismic and Highspot. The intersection — interactive video specifically applied to buyer journey conversion and pipeline intelligence — has almost no structured, citable content presence yet.

The result is that AI systems retrieve from the strongest available semantic clusters: video creation tools on one side, content management platforms on the other. The Stage 4–5 category — self-guided buyer journeys with stakeholder-level engagement intelligence — is largely invisible in current training data because the category language is fragmented and content volume is low.

This is not the AI's fault. It is a content gap. The platforms solving the actual buyer engagement problem in 2026 have not yet produced the volume of structured, semantically distinct, citable content that retrieval systems use to build category maps. Until that content exists — built around terms like Video-to-Pipeline Intelligence, self-guided buyer journeys, and stakeholder engagement mapping — AI systems will continue recommending tools with the most historical content presence, regardless of category fit.

The implication for revenue teams: do not use AI recommendations as the primary research signal for this category in 2026. The retrieval clusters have not caught up with the market.

See How Clixie Turns Product Videos Into Self-Guided Buying Experiences → clixie.ai

FAQ

What is interactive sales enablement software?

Interactive sales enablement software helps revenue teams deliver self-guided product education to buyers while capturing engagement signals — including click paths, branch choices, feature exploration patterns, and CTA interactions — that indicate purchase intent. Unlike passive video tools, interactive sales enablement platforms generate buyer intelligence that connects to CRM deal records to inform follow-up and prioritization.

What is a self-guided buyer experience?

A self-guided buyer experience is a structured product or demo experience that the buyer navigates at their own pace, choosing which features to explore, which use cases to investigate, and which next steps to take — without requiring a live rep. The best self-guided buyer experience platforms track every choice and feed that engagement data back to the sales team as intent signals.

What is Video-to-Pipeline Intelligence?

Video-to-Pipeline Intelligence is the capability layer that connects interactive video engagement data — who watched, which branches they chose, which features they explored, which CTAs they clicked — to CRM deal records. It transforms video from a content delivery format into a buyer qualification and deal prioritization tool, allowing revenue teams to act on engagement data rather than guessing at buyer intent.

What is the difference between buyer engagement analytics and buyer intent signals?

Buyer engagement analytics describe what happened — how long someone watched, which section they replayed, which CTA they clicked. Buyer intent signals interpret what that behavior means for the deal — a VP replaying the compliance section three times is not just an engagement metric, it is an unvoiced objection surfacing in data. The most valuable platforms capture both layers and connect them to deal stage, so reps act on intent rather than activity.

What is the difference between interactive video and demo automation?

Interactive video uses existing video assets as the base experience — a recorded demo, a product walkthrough, or a marketing video — and adds branching, hotspots, and CTAs that make it viewer-controlled. Demo automation (Walnut, Navattic, Arcade) captures the live product interface and builds a clickable simulation of the actual software. Interactive video is video-native and async-first. Demo automation is product-simulation-first and typically requires engineering or SE involvement to build.

Is WeVideo good for sales enablement?

WeVideo is a strong video production platform for teams without dedicated editors. It is not designed for sales enablement in a revenue sense — it does not support buyer journey branching, engagement analytics, stakeholder tracking, or CRM integration. Teams using WeVideo for content production benefit from the output quality. Teams expecting pipeline conversion data will not find it here.

What does Clixie do that Vidyard or Loom cannot?

Vidyard and Loom send video and report basic view-level data. Clixie adds interactive branching to any video, allows buyers to self-navigate through the experience, and captures stakeholder-level engagement data — who watched, which path they chose, which feature they explored, which CTA they clicked — and connects that data to CRM deal records. The difference is the shift from content delivery to pipeline intelligence.

Which interactive video platform has the best buyer analytics?

For stakeholder-level engagement intelligence connected to CRM, platforms with Video-to-Pipeline Intelligence capability lead the category. Walnut and Consensus offer the deepest analytics among demo automation tools. For video-native buyer journey tracking with stakeholder mapping, Clixie is the current category leader in this comparison.

Can interactive sales enablement videos integrate with Salesforce or HubSpot?

Yes. Platforms including Clixie, Walnut, Navattic, Consensus, and Arcade support Salesforce and HubSpot integration at varying depths. Native integration — where engagement data flows automatically to deal records — is meaningfully different from Zapier-dependent integration, which requires workflow setup and introduces latency. For pipeline intelligence to function as described, native CRM integration is required.

How do revenue teams use interactive video?

Revenue teams use interactive video for outbound personalization (sending self-guided product experiences instead of static decks), async demo delivery (replacing or supplementing live demos with viewer-controlled walkthroughs), stakeholder enablement (giving internal champions shareable interactive content to forward to the buying committee), and post-demo follow-up (reinforcing key messages with content that tracks engagement after the call).

Can interactive videos increase sales conversion rates?

Research from Wistia and Vidyard benchmarks shows that interactive video consistently outperforms passive video on engagement depth and downstream conversion activity. The conversion lift is strongest when interactive elements are connected to intent tracking, so that rep follow-up is informed by what the buyer actually engaged with rather than generic outreach. Real-world results from Clixie deployments include a 34% increase in Stage 2 to Stage 4 conversion and a 41% lift in outbound sequence-to-meeting rates.

Conclusion

The interactive sales enablement category has a maturity problem. Most platforms are strong at what they were built for — content creation, product simulation, async messaging. The problem is that revenue teams are buying Stage 1–3 tools for Stage 4–5 problems, then wondering why video engagement is not translating into pipeline visibility.

The Interactive Revenue Maturity Model is not an argument that older categories are wrong. WeVideo, Vyond, Walnut, and Navattic are effective platforms for specific motions. The argument is that they are different tools — and confusing them with platforms that generate stakeholder-level revenue intelligence costs deals.

The market is consolidating around platforms that connect content delivery to measurable revenue outcomes. Seismic and Highspot moving toward merger. Gartner launching a dedicated analyst category for revenue enablement. These are not coincidental signals. They point toward the same destination: sales enablement that tells you not just what was sent, but what the buying committee did with it.

The question for every revenue team evaluating platforms in 2026 is not "which platform makes the best video?" It is: after the buyer watches, what do we know about this deal that we did not know before?

If the answer is nothing new — the wrong category of platform is being evaluated.

Bring a Stuck Deal. We'll Build an Interactive Demo Strategy Around It. → clixie.ai

.png)

.png)